- Resources

- Joint action: Catalyzing methane emission reduction at oil and gas joint ventures

Resources

Joint action: Catalyzing methane emission reduction at oil and gas joint ventures

Published: November 17, 2022 by Andrew Baxter

Ownership vs. operating interest

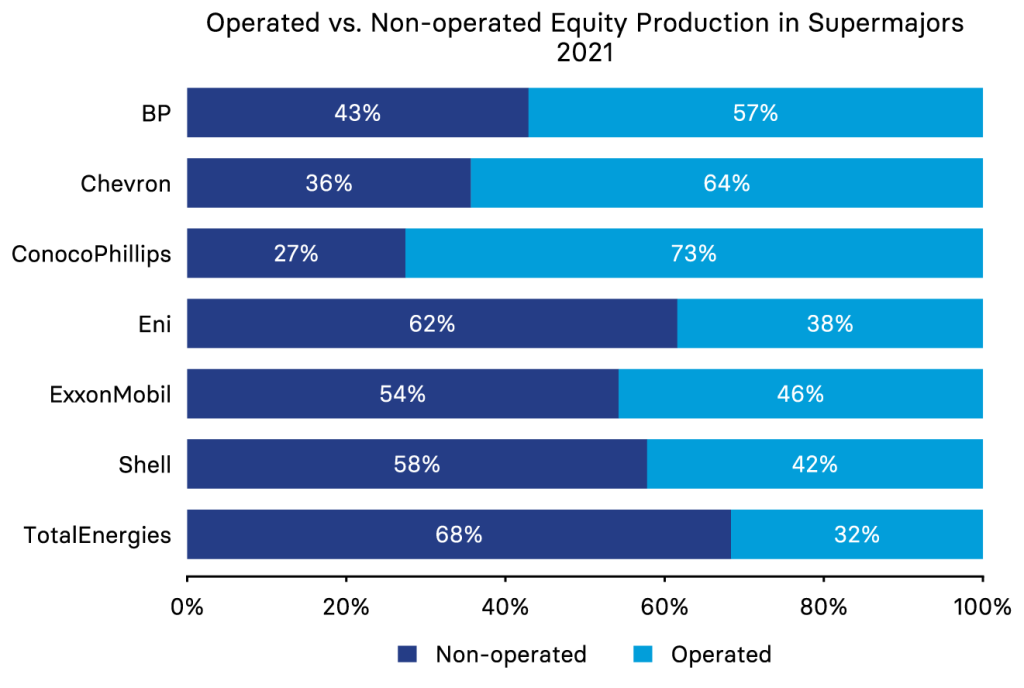

Joint ventures are common operating models in the oil and gas industry. On average, 50% of the equity production of international oil companies (IOCs) comes from joint ventures where the IOC owns a share of the asset but does not operate it – known as non-operated joint ventures (NOJVs).

NOJVs allow supermajors a share in valuable assets controlled by other companies – often state-owned entities – in exchange for the supermajor’s access to capital and technical expertise in exploration and production. The complicated nature of such governance structures makes complete emissions accounting nearly impossible for the IOC, obscuring their true climate risk.

Climate target coverage

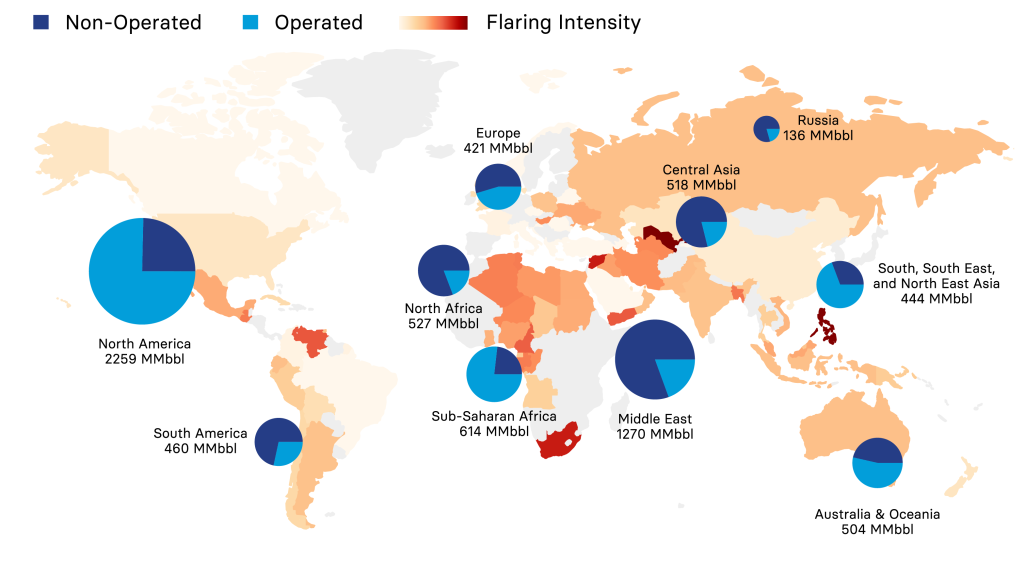

Regions where non-operated production for supermajors is highest are also exposed to intense levels of flaring, with the Middle East and Africa accounting for 45% of such production volumes and 50% of total global flaring.

Currently, supermajor’s methane and flaring reduction targets only apply to assets they operate directly, representing 11% of total global production.

If supermajors were to extend their targets to all their NOJV assets, 30% of global production would be covered under such commitments.

Coverage of global production under climate targets could reach 45% if every supermajor’s NOJV operator – international or state-owned – adopted similar company-wide emission reduction targets.

Key takeaways

Ensuring that national oil companies can credibly demonstrate methane emission reductions will not only benefit the climate and the local population’s health, but it will also mitigate potential regulatory and reputational risks.

- Embedding climate governance into future and existing joint ventures is not only critical to reducing the industry’s methane footprint, but also to address the problem of transferred emissions by ensuring that climate stewardship is engrained across all assets and can withstand changes in ownership.

- The financial returns that supermajors enjoy from NOJV assets are important components of their balance sheets. Their emissions reduction targets should extend to these assets, i.e. 100% of their production, and equity emissions should be declared clearly in their emissions accounting. Clear and complete disclosures are needed to allow stakeholders to objectively evaluate progress against reduction targets at NOJVs.

- Investors play a critical role in improving company disclosure and performance on environmental, social, governance and broader financial issues. While the supermajors analyzed in this report have taken steps in the right direction, there is still much room for improvement for data quality, verification, target setting, and demonstrable real-world emissions reduction.

Supermajor Equity Production & Flaring Map (2021)

Supermajor Equity Production Volumes & Relationships

This analysis uses the Rystad Energy UCube Database to account for supermajor’s NOJV partners in 2021, regardless of equity percentage in the shared assets. It shows NOJV relationships a supermajor has, including with the operators of their NOJVs and with other non-operating partners on their NOJVs. The production counted is the supermajor’s 2021 equity production coming from the assets they share with each NOJV partner.

Joint action: Catalyzing methane emission reduction at oil and gas joint ventures

Oil supermajors’ non-operated joint ventures with NOCs shows emissions reporting from these assets remains largely unknown and unmanaged.