- Resources

- Affordable abatement: Sharpen the focus on flaring

Resources

Affordable abatement: Sharpen the focus on flaring

Published: March 2, 2022 by EDF Staff

By Andrew Howell and Dominic Watson

This post first appeared in Energy Monitor.

Not all greenhouse gas (GHG) emissions are hard to fix. For the oil and gas industry, an early point of focus has been flaring – which largely takes place when natural gas unearthed during oil production is burned as a waste stream. As investors push energy companies to show progress on climate performance, ending this wasteful and polluting practice is a low-cost, high-impact means to deliver results.

As we showed in The Burning Question, our investor guide to the issue, flaring is likely responsible for more than 1% of global GHG emissions (1 gigatonne of CO2 equivalent or more), but most flaring can be avoided through focused planning and management. As J.P. Morgan Asset Management has observed, “flaring is a problem with multiple solutions and a compelling long-term economic proposition.”

The US Environmental Protection Agency is revising federal methane emissions regulations and preparing to issue a supplemental rule next month, potentially including provisions to address flaring. Meanwhile, the Bureau of Land Management is also working on new regulations to limit methane waste on federal and tribal lands. Both should include a ban on all flaring except during emergencies. Operators and investors have encouraged policymakers to take action on the issue; companies that are not already shrinking their flaring footprint risk falling behind and losing revenue.

A new report from Rystad Energy, commissioned by EDF, sheds fresh light on US flaring and the potential to curb it. The report finds that some flaring fixes – especially pipeline gathering and on-site gas use – can turn a profit for operators after accounting for revenues from captured gas. For example, in the Permian Basin, Rystad found that ExxonMobil, Chevron and Shell voluntarily brought flaring rates down to 0.5% or less in 2021, in part through the resolution of timing and coordination issues.

Rystad makes two key points that support accelerated action from oil and gas operators.

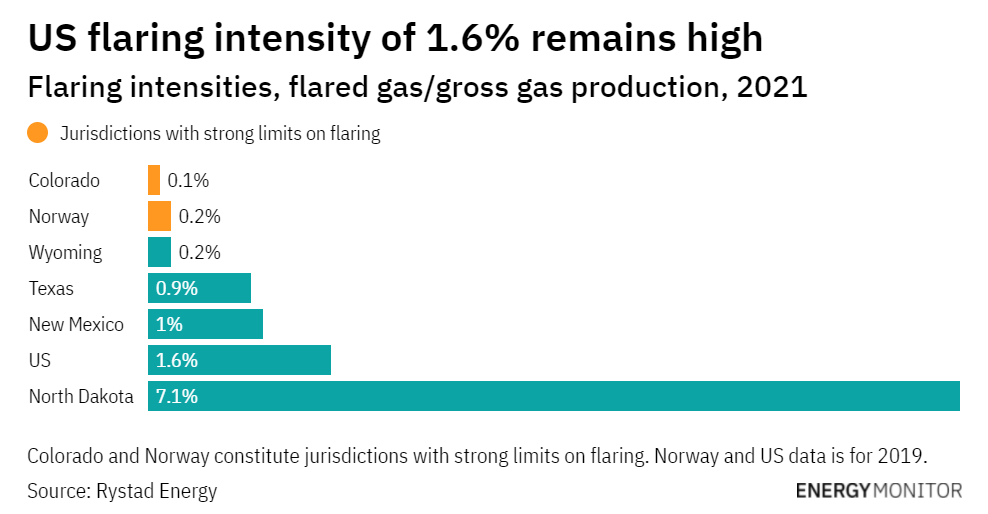

In the US, flaring volumes could fall significantly further. Flaring volumes dropped 30% in 2020 and held flat last year, having surged in the previous decade. However, 700 million cubic feet of gas is still being flared each day – worth well over $1bn a year. The overall US flaring intensity of 1.6% far exceeds what is necessary.

While some minimal flaring in oil and gas operations is unavoidable for safety reasons, rigorous flaring policy is effective – in Colorado and Norway flaring intensity is below 0.2%. In fact, Rystad concluded that flaring above 0.2% is excessive, based on observed flaring in the US and elsewhere.

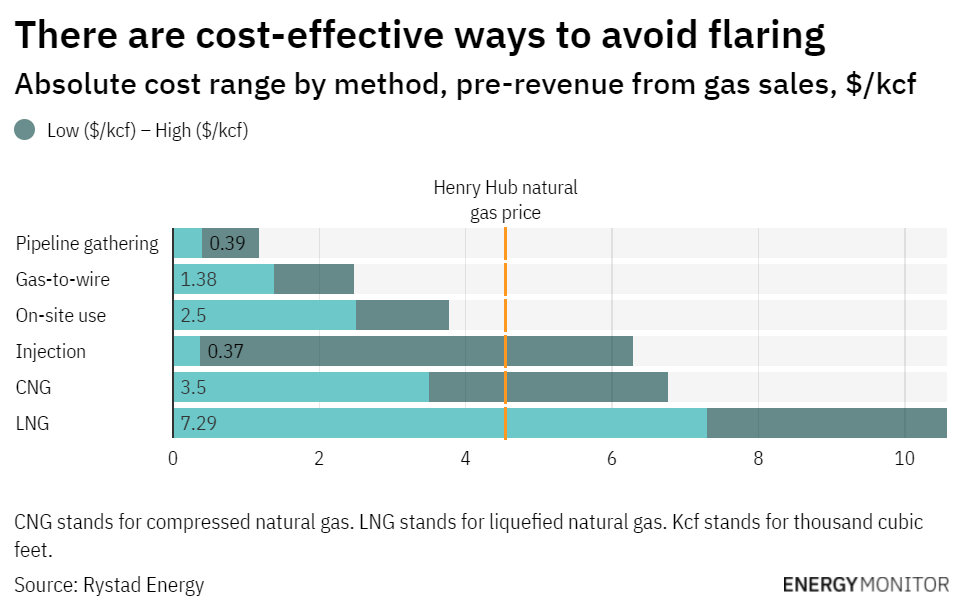

There are cost-effective ways to avoid flaring. The report says most flaring is not inevitable but results from planning gaps such as a lack of gas transport capacity or delays in connecting oil wells to gas infrastructure. There is no one solution to flaring, which is highly site-specific, but in most cases, flaring abatement is cost-effective when accounting for the price of captured gas.

The report also notes that operators that have been most successful in reducing flaring tend to share a mindset in which flaring is seen as a constraint to be avoided, rather than part of normal operations.

Encouraging signs of rising ambition

Since we published The Burning Question, a number of oil producers have announced more ambitious flaring targets. These include Shell, which brought forward its global zero routine flaring commitment for operated assets from 2030 to 2025, and ExxonMobil, which has committed to zero routine flaring in the Permian Basin by the end of this year.

Among US independents, Hess has endorsed the World Bank’s Zero Routine Flaring by 2030 initiative with a goal of eliminating routine flaring from its operations by the end of 2025 – a noteworthy ambition given that Hess has been one of the highest-flaring companies among the large US independents, in our analysis.

These are welcome developments, but investors should ask for more from the industry.

As we have argued, all oil and gas companies should commit to: 1) eliminating routine flaring by no later than 2030 globally and by 2025 in the Permian Basin; 2) set an ambitious target for overall flaring intensity; 3) enforce a zero-tolerance policy for unlit/malfunctioning flares; and 4) support government policies to reduce flaring, including the Environmental Protection Agency’s proposed methane rules.

While methane controls have wide-ranging support, parts of the industry have sought to undermine efforts to eliminate venting and flaring. Finally, investors should also ask for clear disclosures, helping stakeholders measure progress on flaring reduction.

New flaring management guidelines can help

Oil and gas operators looking to do more on flaring abatement have a range of resources to support them. New flaring management guidance from the International Association of Oil & Gas Producers and the World Bank’s Global Gas Flaring Reduction Partnership reviews a range of flaring management strategies and technologies, while providing examples of successful strategies companies have used to reduce flaring – including projects from Petronas in Malaysia, Shell in the Permian and Eni in the Congo.

Today’s publication of the International Energy Agency’s Global Methane Tracker 2022 serves as another important reminder of the importance bringing down emissions that oil and gas operators can control. An abundance of data, analysis and evidence from the field makes clear: oil and gas operators can achieve significant emissions reductions through cost-effective anti-flaring measures. It is time for companies to use the tools at their disposal to fix their own flaring and support strong industry-wide regulations.