Inflation Reduction Act Activation Guide: Fleet Electrification

Fleet Electrification

Inflation Reduction Act Activation Guide

Produced by EDF in collaboration with ![]()

The Inflation Reduction Act (IRA) is a gamechanger for companies that own, operate, or rely on vehicles and aim to reduce their transportation emissions while creating financial value for their businesses.

Companies in these industries tend to own the largest commercial fleets, but any company that owns, operates, or relies on vehicles can benefit from the IRA for fleet decarbonization – including those that work with upstream and downstream transportation partners.

Logistics

Transportation

Retail

Consumer Products

Technology

Telecommunications

Waste Management

Construction

Sources: Deloitte Analysis, 2022 Largest 500 Commercial Fleets

Key Relevant Provisions

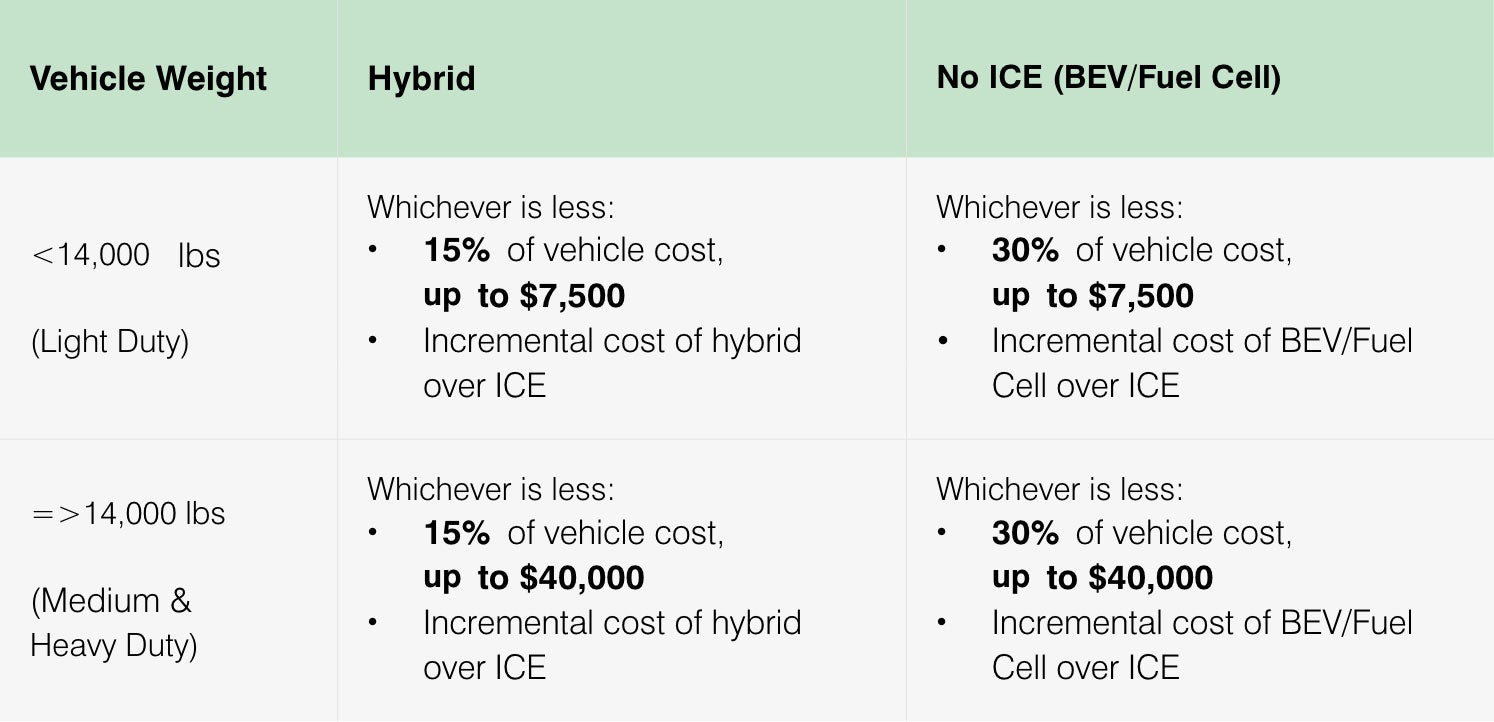

§45W and §30C are key provisions for companies’ transition to clean vehicles, offering up to $40,000 for commercial clean vehicles and up to $100,000 for alternative fueling property.

§45W: Credit for Qualified Commercial Clean Vehicles

Provision

Provides a tax credit for up to $40,000 per vehicle for new purchases of commercial clean vehicles (BEV, PHEV, FCEV), depending on vehicle weight and hybrid vs. BEV.

Key Takeaways

- Covers pure battery electric vehicles (BEVs), hybrids (PHEVs), and fuel cell (hydrogen) powered vehicles (FCEV)

- Does not include restrictions related to income and North American manufacturing and assembly, such as those included in consumer vehicle credit (§30D)

- Total cost of ownership for battery electric vehicles may now be lower than that of diesel trucks, particularly for shorter/local routes, which will accelerate electrification

- Fuel cell trucks will likely still be more expensive than ICE trucks in the near-term

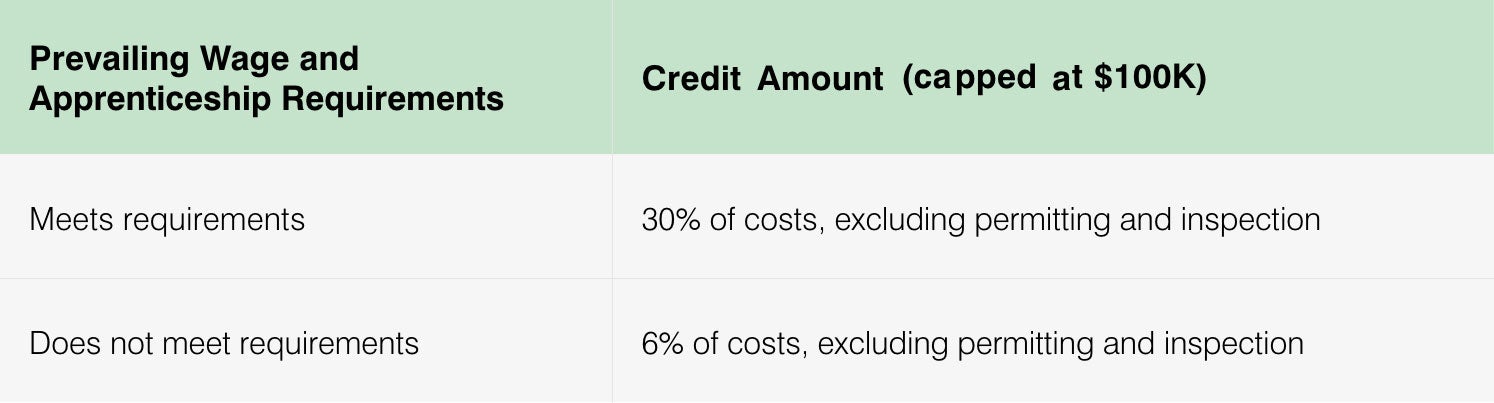

§30C: Alternative Fuel Vehicle Refueling Property Credit

Provision

Provides a tax credit for 6% or 30% of the cost (credit capped at $100,000) of refueling and charging stations for alternative fuels such as electricity, hydrogen, and biodiesel.

Key Takeaways

- Covers three types of fuel: 1) electricity, 2) fuel where at least 85% of volume consists of ethanol or natural gas, CNG, LNG, LPG, or hydrogen, and 3) Diesel/biodiesel/kerosene mixtures where at least 20% of volume consists of biodiesel

- 30% credit for meeting prevailing wage and apprenticeship requirements, 6% otherwise

- Likely most economically viable for on-site charging of large EV fleets or installing on-the-go charging infrastructure

- Includes bidirectional charging which improves the business case for fleet conversion with Vehicle-to-Grid (V2G) in which vehicles sell electricity back to the grid

Notes: Unless otherwise specified, all references to “Section” in this presentation are to the Internal Revenue Code of 1986, as amended (IRC).

Sources: Deloitte Analysis, P.L. 117-119, WH IRA Guidebook, IRC.

The Business Case (Light Duty)

With incentives, all light duty clean vehicle types are now projected to be cheaper than conventional fuel gasoline over 15 years of ownership.

Light Duty: Estimated 15-year Total Cost of Ownership (TCO) for Light Duty Vehicles in the US (Medium SUV) in $, beginning in 2025.

Sample Business Case

Additional cost and revenue drivers to consider include vehicle depreciation, vehicle lifespan, vehicle resale value, charging infrastructure, actual state and local incentives based on geography, and cost of capital. See IEA TCO tool for calculation support.

A company with 100 light duty vehicles could save an estimated $1,600,000 over 15 years by converting from conventional fuel gasoline vehicles to clean vehicle alternatives based on total cost of ownership differences.

Assumptions

- All TCO data is from 2021 Argonne National Lab Study with two exceptions:

1) Downward adjustment to battery cost estimates for BEV300 and PHEV based on projected impacts of IRA ($82.5/kWh)

2) Added estimated IRA tax credit value - 15-year ownership assumes an estimated 201,400 miles in Argonne study

- Assumes PHEV Battery Capacity is >7 kWh

- Impact of IRA credit on vehicle depreciation value is not included in analysis, IRA and state credit values are not tax-impacted

- MSRPs based on 2025 model year prices

- IRA credit is absorbed by purchaser entirely

- Other changes to battery pack manufacturing costs (e.g., through IRA labor requirements) were not considered

- Finance costs likely to be lower than estimated due to IRA tax credit

- Excludes IRA effect on fuel and charging prices

- Total cost savings in sample business case is based on lowest cost clean vehicle option (FCEV)

- Estimated state incentive values are blended national averages by powertrain type (BEV/PHEV/FECV) of ($7,578/$6,311/$10,114)

Sources: Deloitte Analysis, Argonne National Lab, ICCT, BNEF 1, BNEF 2, DOE State Incentives Database, IRC.

The Business Case (Medium Duty)

With incentives, all medium duty clean vehicles are now projected to be cheaper than conventional fuel diesel over 15 years of ownership.

Medium Duty: Estimated 15-year Total Cost of Ownership (TCO) in the US (Pickup/Delivery) in $, beginning in 2025.

Sample Business Case

Additional cost and revenue drivers to consider include vehicle depreciation, vehicle lifespan vehicle resale value, charging infrastructure, actual state and local incentives based on geography, and cost of capital. See IEA TCO tool for calculation support.

A company with 100 medium duty vehicles could save an estimated $5,600,000 over 15 years by converting from conventional fuel vehicles to clean vehicle alternatives based on total cost of ownership differences.

Assumptions

- All TCO data is from 2021 Argonne National Lab Study with two exceptions:

1) Downward adjustment to battery cost estimates for BEV150 and PHEV based on projected impacts of IRA ($82.5/kWh)

2) Added estimated IRA tax credit value - 15-year ownership assumes an estimated 201,400 miles in Argonne study

- Impact of IRA credit on vehicle depreciation value is not included in analysis, IRA and state credit values are not tax-impacted

- Assumes PHEV Battery Capacity is >15 kWh

- MSRPs based on 2025 model year prices

- IRA credit is absorbed by purchaser entirely

- Other changes to battery pack manufacturing costs (e.g., through IRA labor requirements) were not considered

- Finance costs likely to be lower than estimated due to IRA tax credit

- Excludes IRA effect on fuel and charging prices

- Total cost savings in sample business case is based on lowest cost clean vehicle option (BEV)

- Estimated state incentive value of $30,439 is a blended national average

Sources: Deloitte Analysis, Argonne National Lab, ICCT, BNEF 1, BNEF 2, DOE State Incentives Database, IRC.

The Business Case (Heavy Duty)

By 2030 or sooner, heavy duty electric and plug-in hybrid vehicles are projected to be cheaper than conventional fuel diesel over 15 years of ownership.

Heavy Duty: Estimated 15-year Total Cost of Ownership in the US (Tractor – Day Cab) in $, beginning in 2030.

Sample Business Case

Additional cost and revenue drivers to consider include vehicle depreciation, vehicle lifespan vehicle resale value, charging infrastructure, actual state and local incentives based on geography, and cost of capital. See IEA TCO tool for calculation support.

A company with 100 heavy duty vehicles could save an estimated $15,100,000 million over 15 years by converting from conventional fuel vehicles to clean vehicle alternatives based on total cost of ownership differences.

Assumptions

- All TCO data is from 2021 Argonne National Lab Study with two exceptions:

1) Downward adjustment to battery cost estimates for BEV300 and PHEV based on projected impacts of IRA ($82.5/kWh)

2) Added estimated IRA tax credit value - 15-year ownership assumes an estimated 201,400 miles in Argonne study

- Impact of IRA credit on vehicle depreciation value is not included in analysis, IRA and state credit values are not tax-impacted

- Assumes PHEV Battery Capacity is >15 kWh

- MSRPs based on 2030 model year prices

- IRA credit is absorbed by purchaser entirely

- Other changes to battery pack manufacturing costs (e.g., through IRA labor requirements) were not considered

- Finance costs likely to be lower than estimated due to IRA tax credit

- Excludes IRA effect on fuel and charging prices

- Total cost savings in sample business case is based on lowest cost clean vehicle option (BEV)

- Estimated state incentive value of $65,305 is a blended national average

Sources: Deloitte Analysis, Argonne National Lab, ICCT, BNEF 1, BNEF 2, DOE State Incentives Database, IRC.

Additional factors and markets trends will likely improve the business case for clean commercial vehicles.

- IRA incentives for battery manufacturing within the US is accelerating the rise of the “Battery Belt,” which will likely help manage EV supply chain costs and risks

- The CHIPS and Science Act provides approximately $280 billion in new funding for domestic research and manufacturing of semiconductors, another key input into EVs, which will likely help ease supply chain bottlenecks

- The IRA is estimated to nearly triple federal tax incentives for green energy over the next ten years

- Boosts in renewable energy supply are projected to result in the lowest levelized cost of clean electricity in the world, which will likely reduce fueling/charging costs for EV owners

- Both public and private investments are significantly expanding the network of affordable and accessible EV charging stations (including bi-directional vehicle charging capabilities)

- The IRA offers additional funding for clean vehicles beyond Sec. 45W and 30C, such as Clean Ports funding and Clean Heavy-Duty Vehicle Program

- The Infrastructure Investment and Jobs Act (IIJA) provides approximately $18.6 billion in funding for EV infrastructure and charging programs

- Many state and local governments provide clean vehicle grants in addition to incentives, and some offer significantly higher incentives than the average values reflected in the TCO analysis

Sources: Deloitte Analysis, Axios, Goldman Sachs, P.L. 117-119, WH IRA Guidebook, White House 1, White House 2, WH IIJA Guidebook

The Climate Case

Converting to clean vehicles can help US companies reduce their fleet emissions by approximately 60%, and approximately 83% on a fully renewable grid.

")

Assumptions

- Fuel and electricity consumption values are based on the EPA data

- Average vehicle lifetime of 18 years and 209,402 miles

- Excludes effect of IRA on renewable energy deployment in the grid, which is likely to improve the climate case

- Excludes IRA effect on fuel and charging prices

- Nitrous Oxide (N2O) emissions are assumed to be 3.2 mg/mile for gasoline and 24.1 mg/mile for diesel based on ICCT data

- Uses light duty vehicle data as a conservative estimate because emissions reduction potential increases as vehicle size / fuel consumption increases

Sample Climate Case

Exact emissions reduction potential will depend on grid decarbonization, charging infrastructure optimization, and vehicle size. Absolute emissions reduction potential increases as vehicle size increases due to the greater fuel consumption of larger vehicles.

A company with 100 light duty vehicles could save an estimated 5,950 MTCO2e over the lifetime of its vehicles by converting from conventional fuel vehicles to clean alternatives.

This estimate includes approximately 67.4 kg of avoided N2O pollution, which would drive significant improvements in air quality and public health outcomes, particularly in disadvantaged communities. Compared to a diesel vehicle baseline, avoided N2O emissions increase to 505.5 kg.

Credit Overview

Provision Description

Provides a tax credit for purchasers of qualified commercial clean vehicles

Period of Availability

Vehicles acquired and placed in service between 1/1/23 and before 12/31/32

Incentive Type

Tax credit for commercial use including lease to third parties and direct pay for tax-exempt organizations

New or Modified Provision

New

Credit Amount

Eligibility Requirements

Organization Types and Usage:

- Businesses that acquire motor vehicles or mobile machinery for use or lease in the US

- Tax-exempt entities that acquire motor vehicles or mobile machinery for use in the US

- Must be for use in business, not for resale (includes leasing to others, e.g., car rental business)

Vehicle Types:

- Not subject to North American manufacturing and assembly requirements included in 30D

- Excludes trains

- Minimum of 7 and 15 kWh battery capacity for hybrids and BEVs under and over 14,000 lbs, respectively

Example eligible vehicles types (non-exhaustive):

- Light Duty (0-14,000 lbs)

- Medium Duty (14,001-26,000 lbs)

- Heavy Duty (26,001+ lbs)

- Mobile Machinery

Available January 1, 2023 through December 31, 2032

How to Claim the Credit

- Monitor IRS website for release of relevant tax form (still finalizing form for businesses to file alongside federal tax return to claim credit and will post here when complete (IRS Forms))

- Review the IRS Guidance on assessing incremental cost and DOE study to compute the anticipated credit amount

- Collect and record vehicles’ VIN along with the amount of the credit to prepare for tax forms

Sources:Deloitte Analysis, P.L. 117-119, WH IRA Guidebook, IRS Commercial Clean Vehicle Credit Overview, IRC.

Credit Overview

Provision Description

Provides a tax credit for the installation of alternative fuel vehicle refueling and charging property by businesses, tax-exempt entities, and individual taxpayers in the US

Period of Availability

Infrastructure placed in service between 1/1/23 and 12/31/32

Incentive Type

Tax credit for personal and commercial installation

New or Modified Provision

Modified and timeframe extended

Credit Amount for Individuals

30% of costs, capped at $1,000 (excluding permitting and inspection)

Credit Amount for Businesses

Eligibility Requirements

Organization Types and Usage:

- Businesses and tax-exempt entities that install a qualified refueling property placed in service in the eligibility timeframe. Fueling station owners who install qualified equipment at multiple sites are allowed to use the credit towards each single item in each location

- Individuals who install a qualified refueling property at their principal residence

Geographic Location:

Property must be placed in an eligible census tract as defined in under Sec. 45D(e), being either:

- Low-Income Community with certain poverty rate and median income requirements; or

- Non-urban area as defined by the Census Bureau

Source: CDFI Fund Mapping Tool

Available January 1, 2023 through December 31, 2032

How to Claim the Credit

- File IRS form 8911 alongside their federal tax return to claim the credit (IRS Forms)

- Explore combining with State Grants for Highway Corridor Charging, State Rebates/Vouchers for Charging Purchases and Utility Make Ready (installation costs), and/or Rebate Programs to further lower upfront costs as well as grants that cover operations and maintenance

- Evaluate stacking 30C with 48/48E for on-site electricity generation and storage

Sources:Deloitte Analysis, P.L. 117-119, WH IRA Guidebook, IRC.

Companies are already taking advantage of the IRA to support their transition to clean vehicles.

Fleet Electrification and Charging Infrastructure Examples

Delivery Fleet Electrification

In December 2022, DHL announced the rollout of 45 (with 130 forthcoming) new last mile delivery vans in Palo Alto, California as part of the company’s commitment to operate 60% of its U.S. vehicles electrically and reduce all logistics emissions to net zero by 2050.![]()

![]()

EV Charging Market Entry

In January 2023, Mercedes-Benz announced plans to launch a global high-power EV charging network across North America, Europe, China, and other key markets. It will begin to be built in 2023 in the US and Canada, followed by other regions around the globe.![]()

Heavy Duty Fleet Electrification

In December 2022, PepsiCo announced the rollout of 100 heavy-duty Tesla Semitrucks in 2023 for deliveries to customers like Walmart and Kroger. Alongside the vehicle purchase, PepsiCo is installing four 750 kW charging stations in California. The IRA commercial vehicle credit and state grants supported the purchase.![]()

![]()

Sample Clean Vehicle Vendors

Class 3&4

Several electric cargo van companies currently operate in the North American market.![]()

![]()

![]()

![]()

Class 5&6

Step van options are improving in terms of availability and performance. Newer market entrants are willing to accommodate custom vehicle specifications.![]()

![]()

![]()

![]()

![]()

Class 7&8

Several class 8 models are expected to enter the North American market with the earliest one being the Volvo VNR by 2023.![]()

![]()

![]()

![]()

![]()

Notes: All information on this slide has been obtained from publicly available sources (e.g., press releases) and shall not be construed to reflect companies’ tax attributes or actual usage of tax credits.

Sources: Deloitte Analysis, DHL, Mercedes-Benz, PepsiCo

Every function has a role to play to take advantage of the IRA to support the transition to clean vehicles.

- Assess fleet decarbonization against corporate strategy

- Analyze competitive landscape to estimate competitors’ movement on clean vehicles post-IRA and protect first-mover advantage

- Calculate projected abatement potential from fleet decarbonization and compare against goals and strategy

- Assess against alternative abatement projects to calculate opportunity cost of investment

- Refresh business case with IRA incentives

- Calculate optimal vehicle type and per-vehicle savings

- Present and receive sign-off on business case from CFO

- Consider effect of depreciation on finances (depreciable basis of the vehicle is reduced by the amount of the commercial clean vehicle credit the company receives)

- Assess eligibility for §45W and §30C based on census tract definitions of low-income and rural communities and calculate projected value

- Prepare to file for relevant credits and incentives (e.g., §45W: track VIN, purchase price, and manufacturer; §30C: IRS Form 8911)

- Work with Finance to identify vehicle and charging needs to inform cost estimates

- Identify specific vehicle and charging manufacturers to purchase from (e.g., Qualified Manufacturers for §45W)

- Identify additional federal, state and local incentive structures

- Engage with the IRS to provide input on credit allocation mechanisms (while the comment period for both credits closed Dec. 3, 2022, the IRS will consider input provided after that date at www.regulations.gov (type IRS-2022-56))

Sources: Deloitte Analysis, IRC.

Resources

The Inflation Reduction Act: A Snapshot for Business

Includes overview, description, and funding details for each IRA funded incentive.

Inflation Reduction Act Activation Guide: Renewable Energy Procurement

The IRA aims to increase supply of renewable energy in the US and is projected to lower clean energy costs in the long-term.

Inflation Reduction Act Activation Guide: Climate-Smart Agriculture

A broad range of companies within the food sector can use IRA-funded agricultural programs to support their climate goals.

Inflation Reduction Act Activation Guide: Building Energy Efficiency

Companies with high energy footprints are most likely to benefit from the IRA’s credits and deductions for energy saving building technologies.

Inflation Reduction Act Activation Guide: Advanced Manufacturing

Any company that owns or sources from industrial facilities may benefit from IRA incentives.Inflation Reduction Act Tracker

The IRA Database compiles information about the climate change-related provisions of the 2022 Inflation Reduction Act (IRA)

IEA Electric Vehicles: TCO Tool

Interactive calculator where users can compare costs of owning and operating ICE vs. electrified vehicles.

EDF Fleet Electrification Solutions Center

Interactive tool with step-by-step guide on fleet electrification.

NACFE - North American Council for Freight Efficiency

Organization that publishes analysis, workshops and data for heavy duty fleet conversion.

IRS Credits and Deductions under the IRA

Includes overview, description, and funding details for each IRA funded incentive.

BGA IRA User Guide

Provides overview of IRA incentives by sector and explains funding mechanisms.

IRS Credits and Deductions under the IRA

Resources, forms and descriptions of IRA tax credits and deductions.Visit the IRA Hub

Credit: Environmental Defense Fund and Deloitte

This document was produced by Environmental Defense Fund in collaboration with Deloitte Consulting LLP. The views within the report are that of Environmental Defense Fund, and do not necessarily reflect the views of report partners or collaborators.This document contains general information only and Deloitte is not, by means of this document, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This document is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this document.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.Copyright © 2023 Deloitte Development LLC. All rights reserved. 36 USC 220506 Member of Deloitte Touche Tohmatsu Limited

Our Experts

Victoria Mills

Managing Director

Environmental Defense Fund

vmills@edf.org

Andrea Pereira

Climate Policy & Outreach

Environmental Defense Fund

apereira@edf.org

Sign up for Climate Policy News you can use

"*" indicates required fields